(Guest Post by Lindsey Burke)

Second grader Nathan is the beneficiary of the new frontier of school choice: education savings accounts. “Two years ago, before the ESA program, Nathan spoke with a lot of jargon and mixed responses,” says his mother Amanda. “Two years ago we weren’t even sure if we were ever going to have a conversation with him. The only reason this is possible is because we could find programs that meet his needs with ESA funds.”

Thanks to Arizona’s pioneering Empowerment Scholarship Account program, which began in 2011, children with special needs like Nathan, as well as children from active duty military families, foster care, and children in underperforming schools can exit the public system and have 90 percent of what the state would have spent on their education deposited into an education savings account. Funds are deposited onto a restricted-use debit card, and parents are then able to direct spending to any education-related service or provider of choice.

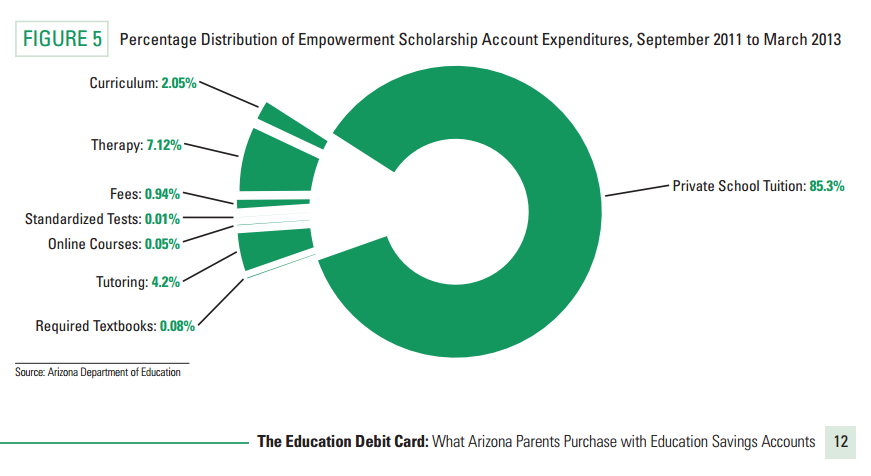

Parents can use ESA funds, deposited into their accounts quarterly, to pay for a variety of education services and providers, including private-school tuition, private tutoring, special education services, homeschooling expenses, textbooks, and virtual education. Parents may also roll over funds from year to year, and can use the money to invest in a college savings plan to pay for college tuition in the future.

I recently evaluated Arizona’s ESA program for the Friedman Foundation to determine the extent to which parents were using their ESAs to actually customize their children’s educational experience. Using data provided by the Arizona Department of Education, I found that more than one third of families used their ESAs to tailor their child’s education, purchasing multiple services and products.

Families use their ESAs to finance a variety of education-related services from a range of providers. One family used roughly 60 percent of their ESA funds for educational therapy, 30 percent for private tutoring, and the remainder of their ESA for curricula. Another family put three-quarters of their ESA dollars toward private school tuition and invested the remaining 25 percent in a college savings fund. A third family divvied up their ESA spending on private school tuition, tutoring, curricula, and online learning.

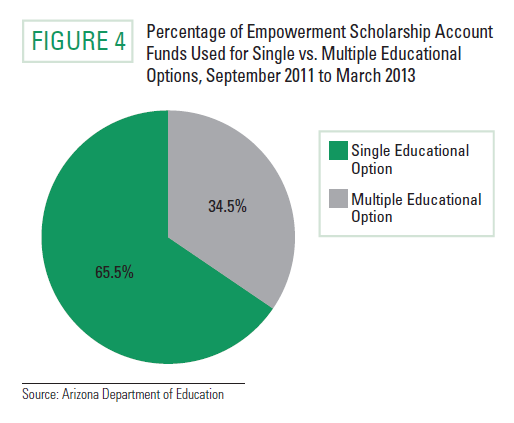

While most families use their ESAs like a school voucher to attend a single private institution that they have chosen, approximately 34 percent use their ESAs to finance multiple education options in a given day. ESAs move beyond the worthwhile goal of choice among schools to choice among education service providers, courses, teachers, and methods—not limited to one brick-and-mortar location.

ESAs are unique in another way: whereas traditional school vouchers must be spent in their entirety, ESAs foster demand-side pressure for education providers to offer more cost-efficient educational services by creating an incentive for parents to shop for education services based in part on cost. Parents are taking opportunity costs into account, saving ESA funds in anticipation of future education-related expenses, including college tuition. During the first quarter of the 2012-13 school year, parents rolled-over 26 percent of their ESA funds.

Arizona has created a model that other states should consider: funding children instead of physical school buildings and allowing funds to follow children to any educational provider of choice. Jonathan Butcher and I also recently detailed how state policymakers could transition more traditional voucher and tuition tax credit programs into flexible education savings accounts. They could:

- Create public school education savings accounts. Parents could use a public school education savings account for traditional school classes, public charter school offerings, public virtual schools such as the Florida Virtual School, community colleges, or state universities.

- Shift existing school voucher or scholarship tax credit funds to an education savings account. States with existing voucher programs or scholarship tax credit programs should allow parents to deposit voucher or scholarship funds into an education savings account in order to gain more flexibility with their child’s funds.

- Expand the approved expenses covered by a voucher or private school scholarship. This would include expanding the uses of a school voucher or scholarship, transitioning the program into an education savings account.

We are entering a new frontier of school choice. Education savings accounts represent an advance and refinement of Friedman’s original voucher concept. Through ESAs, Arizona is moving beyond school choice to education choice. Kym Wilber, whose son Zach is an ESA recipient, explains:

“I use Zach’s ESA funds for other things than just tuition. Because Zach is more on the moderate to severe functioning level [in terms of special needs], his funding can be used more broadly. I have a private tutor for Zach, and I can use the (ESA) funds for that. With the ESA, I can actually go out and buy things for our home program, such as additional speech tools.”

Providing that level of customization to every child would bring American K-12 education into the 21st century and ensure no child is relegated to the existing monopolistic system in which limited effectiveness is all too prevalent in states across the country.

[…] But despite these setbacks, the trend as a whole seems to be in favor of greater school choice. One successful program in Arizona has been getting some excellent legal headway in terms of whether or not the program is […]